Steps Doctors Can Take To Protect Themselves and Their Family Financially (and Otherwise)

- Jan 25

- 10 min read

Physicians spend their careers helping protect their patients, but many unintentionally leave gaps when it comes to protecting themselves and their families. Having a high earning potential, as well as the nature of patient care, can lead to increased liability exposure, creating a unique risk profile for doctors. Obviously, as physicians we know better than most that you can’t predict the future, but preparation can help prevent the worse case from happening. Below, we cover critical areas every doctor should address to minimize risk and ensure their family is protected to the best of their ability.

Disclosure/Disclaimer: This page contains information about our sponsors and/or affiliate links, which support us monetarily at no cost to you, and often provide you with perks, so we hope it's win-win. These should be viewed as introductions rather than formal recommendations. Our content is for generalized educational purposes. While we try to ensure it is accurate and updated, we cannot guarantee it. Rules/laws can change frequently. We are not formal financial, legal, or tax professionals and do not provide individualized advice specific to your situation. You should consult these as appropriate and/or do your own due diligence before making decisions based on this page. To learn more, visit our disclaimers and disclosures.

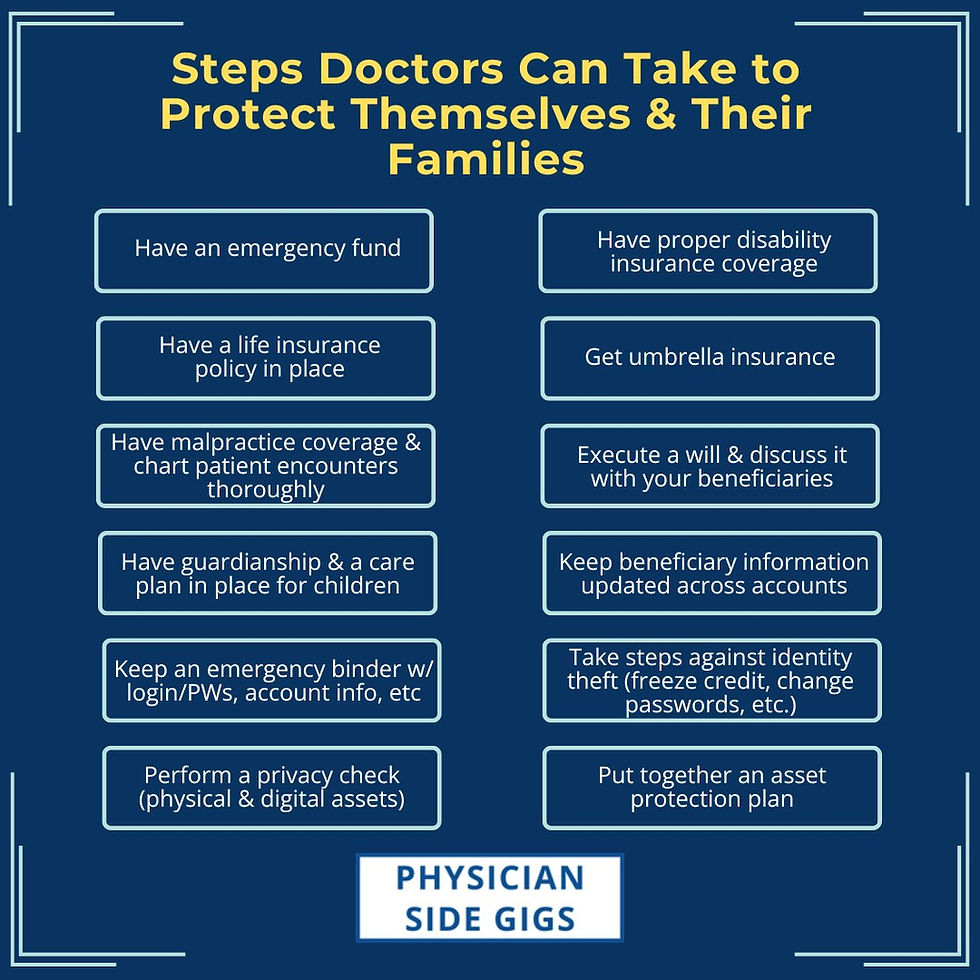

Build (and maintain) an adequate emergency fund

Having an emergency fund is your family’s first line of defense financially. Having liquid cash available ensures that unexpected expenses don’t derail your finances or leave you in a bind where you have to borrow money from family or friends or secure a personal loan. This covers things like unexpected unemployment, large medical bills, or an expensive roof repair.

We typically recommend having 3-6 months of expenses saved and earmarked solely for an emergency fund. At the beginning of your career, or in times of financial or career instability, err on the side of caution and save on the higher side. Depending on the degree of risk aversion, some physicians may keep up to 12 months of expenses in their emergency fund.

Keep this in a short-term investment that’s easy to access, such as a money market fund or a high-yield savings account or high-yield cash account.

Related PSG resources:

Carry proper disability insurance to protect your income & financial future

The ability to earn an income is one of the greatest assets doctors have. Disability insurance helps protect that earning potential, and is one of the staples of physician personal finance. It’s important to have true own-occupation coverage through an individual policy that can follow you throughout your career from job to job. Employer-sponsored and other group plans can be a supplemental or backup option if you’re at risk for getting denied a policy due to medical underwriting, but shouldn’t be your first line of defense. Underwriting for disability insurance gets harder - and more expensive - as you get older, so should be tackled early in a doctor’s career.

How much disability coverage you need depends on your situation and your lifestyle. Residents and fellows should typically take the max benefit offered (usually around $5,000/month) while attending physicians often look for $10,000-$15,000 per month in benefits.

Work with an independent disability insurance broker to compare your options across the major carriers that offer own-occupation coverage and to discuss potential policy riders. Thousands of our members have used and said positive things about our sponsors on our page of disability insurance agents for doctors.

Related PSG resources:

Have enough life insurance in place to protect your family

Sadly a lot of physician families find out too late that they’re underinsured for the lifestyle they live, and in the majority of physician families, the physician is the primary breadwinner. Similar to disability insurance, group life insurance plans–often offered by employers–typically don’t provide enough coverage to protect your family in the unfortunate event of your death.

Make sure you have a term life insurance policy that allows your family to live the life you want for them in the event that you can no longer provide for them financially. How much life insurance coverage a physician needs depends on many factors, but when polled, most physicians on our online communities carry between 3-5 million in life insurance at early stages of their careers. Additionally, the amount you require will change as your career progresses, secondary to increased savings as well as dependents growing older and debts such as mortgages being paid off. Therefore, laddering your life insurance policies will allow you to save on premiums while providing adequate coverage for each stage of your life.

Independent insurance brokers have access to knowledge and discounts to help you get the best priced policy. Our sponsors, including PolicyGenius, have helped thousands of doctors get proper coverage in place. See our recommended life insurance agents for physicians.

Related PSG resources:

Have umbrella insurance in place for additional protection, especially against large or frivolous lawsuits

Physicians are often targets of larger lawsuits secondary to perceived wealth. Umbrella insurance is an often overlooked protection that provides an extra layer of liability protection on top of your existing auto and homeowners policies. It typically covers claims or expenses relating to personal property damage, bodily injury liability, landlord liability for rental properties, defamation of character, and legal costs associated with covered claims. Notably, it does NOT wrap around malpractice lawsuits.

How much umbrella insurance coverage you need depends on how much in assets you have to protect (and your primary home and auto policies may need to be at a certain amount before you’re eligible).

Related PSG resource:

Protect yourself from malpractice exposure

Medical malpractice’s exemption from umbrella insurance helps highlight the importance of having proper malpractice coverage in place, both for your main job and any side gigs you have. Confirm that all your side gigs, such as consulting, telemedicine, a micropractice, and locums work are covered by your existing policies. If they aren’t, get proper coverage in place immediately. If you have a claims-made policy, ensure you have continuous coverage with proper nose or tail coverage.

Along with having appropriate coverage in place, make sure you chart your patient encounters thoroughly and appropriately so you have documentation to protect you. You’ll also of course to invest time into developing good relationships with your patients, as this has been shown time and again to prevent lawsuits.

Related PSG resources:

Have a will in place and discuss it with your family and other beneficiaries

A last will and testament is the most common document people think about when it comes to estate planning, and it can help protect the transfer of assets to your intended beneficiaries without having to go through a long and expensive probate process. Your will also dictates who is responsible for executing your estate plan, so it’s important to discuss the responsibility and the contents of your will accordingly. Getting everyone on the same page now can help family members navigate a highly emotional time in the event of your passing.

Related PSG resources:

Have guardianship & a care plan in place for any children

As part of a will, you can denote legal guardianship for minor children. If you have children, this decision is a critical protection to have in place. It’s also a large responsibility for a guardian, so make sure this is discussed ahead of time with the related parties to ensure the prospective guardians are comfortable with the role and are financially and emotionally capable of handling it.

You may wish to consider establishing a trust to help manage assets and inheritances for minor children. While a will can direct how assets are distributed, a trust offers more control over when and how assets are transferred. This can be especially important for children with special needs who may require long-term care.

Related PSG resources:

Keep your beneficiaries updated everywhere

Outdated beneficiaries are one of the most common–and potentially costly–mistakes doctors make when putting together a plan to protect their family’s financial future. A will can help direct beneficiaries for many common assets, such as bank accounts and homes. Certain assets and other protections, such as retirement accounts, have beneficiaries linked directly to the account or policy.

Review your beneficiaries on your:

Life insurance policies

Retirement accounts (such as your 401(k) and IRA)

Bank and brokerage accounts

Will and trust documents

Situations that can trigger a need to update your beneficiaries include:

Marriage

Divorce

Birth of a child or other family member

Death of a family member or other benefactor

These can all be times of great joy or grief, and legal paperwork may be the last thing on your mind, but it’s important to keep your beneficiaries current to save your family unnecessary additional stress in the future.

Create an emergency binder

An emergency binder is a collection (either physical or digital) of critical personal, financial, and medical documents with emergency contacts and instructions. Having one in place allows your loved ones or caregivers to manage your affairs to your wishes and without delay. Your emergency binder should include:

Information on your insurance policies

Account information (retirement, bank, utilities, and even subscriptions) & passwords for accounts

Passwords for devices

Emergency contacts & other important contacts (financial advisor, attorney, employer, etc.)

Information about your properties (primary residence, vacation homes, investment properties, etc.)

Other important information (pet care, childcare, medical information, wishes for your memorial service, etc.)

Given the sensitive information collected in the emergency binder, make sure this is stored in a secure location, but that your family knows how to find and access it.

Related PSG resource:

Our partners offer a Family Emergency Binder that’s clean/easy, comprehensive, and preorganized. At under $40, it's probably one of the best steps you can take to ensure somebody can take over your affairs if necessary. There is a money back guarantee from the creator if it's not what you want.

Put protections and guardrails in place against identity theft

High income individuals are frequently the targets of identity theft and fraud. There are several different steps doctors can take to help protect themselves:

Freeze your credit with all three of the major credit bureaus

Change your passwords regularly

Monitor your accounts and credit reports for any unusual or unauthorized activity

Get identity theft protection coverage/insurance

Related PSG resource:

Perform a privacy check of physical and digital assets

Another way to protect yourself from potential threats is to make it more difficult for potential spammers to find information about you. Your professional and personal visibility can make you and your family a more attractive target for scams, lawsuits, and even harassment.

A privacy check should include:

Reviewing what personal information is publicly searchable (home address, phone number, family details, etc.) and taking steps to limit or protect this information, such as using a Google voice number instead of your personal cell phone, getting a post mail box to list and use for a mailing address instead of your home address, getting a EIN instead of using your social for 1099 work, putting your home in a trust to help shield your home address in public records, etc.

Reviewing what you share on social media accounts, as well as your privacy settings on who has the ability to view what you post

Being cautious about professional listings, online bios, etc. and ensuring they don’t disclose unnecessary personal information

Opting out of data broker sites that sell your personal information

Have a comprehensive asset protection plan in place

Given the higher than average liability exposure doctors face, titling and protecting your assets intentionally before a problem arises can help protect you and your family in a worst case scenario.

We’ve touched on a few key items such as the insurance coverages above, but an effective asset protection plan can also include:

Putting retirement savings into ERISA protected accounts that are not subject to lawsuits

Putting rental properties and other real estate assets into LLCs

Separating business and personal assets to help limit liability

Ensuring assets are titled correctly (personal vs business, individually vs jointly owned)

We cover this in greater detail in our guide to asset protection strategies. Your asset protection plan isn’t a one-time consideration. Asset protection is a proactive measure, and your strategy can change as you secure additional assets and as your assets grow in value.

Related PSG resource:

Anderson Advisors offers a comprehensive suite of asset protection services, including planning, registered agent, and entity formation. Our affiliate link will get you a free strategy session to discuss these issues and explore what's right for you, as well as give you access to packages at a discounted rate.

Conclusion

You’ve worked hard to build your career and to provide yourself and your family with a lifestyle that meets your goals and needs. While not all risks and exposure can be prevented, taking proactive steps now can help limit the risk and help ensure that your family remains secure, supported, and protected. With the above foundations in place, you can not only provide protection but gain peace of mind and provide clarity to your family

Related resources for physicians

Explore related PSG content:

Sign up for our weekly newsletter for alerts on free webinars for related personal finance topics and access to new related member perks.