How to Choose the Best Life Insurance Company and Policy

- Apr 23

- 6 min read

Almost all physicians in our online communities for doctors find that they need to purchase life insurance at some point in their careers, and one question that often comes up while shopping policies is how to determine what the best life insurance company is. Unlike other types of insurance, the decision about what life insurance company or policy to choose is often pretty straightforward as there aren’t as many options tied to a policy, particularly if you’re shopping term life insurance (which is what’s usually the best financial option for most physicians). That said, there are a few things you should make sure you know about the company whose policy you choose in order to feel confident that you are making the right decision. We’ll cover those below.

Disclosure/Disclaimer: Our content is for generalized educational purposes. While we try to ensure it is accurate and updated, we cannot guarantee it. We are not formal financial, legal, or tax professionals and do not provide individualized advice specific to your situation. You should consult these as appropriate and/or do your own due diligence before making decisions based on this page. To learn more, visit our disclaimers and disclosures.

Article Navigation

What is the financial strength of the life insurance company, and what are its ratings?

What is the cost of the policy, and does the price reflect the value of the life insurance benefit?

Do a quick search for reviews and complaints of the life insurance companies you’re leaning towards

Additional personal finance and life insurance resources for physicians

Does it matter which life insurance company you choose, and is there a 'best' company?

For the purposes of this article, we are mostly going to assume that you are buying term life insurance, which is what most physicians need, as opposed to permanent life insurance. Permanent life insurance products such as whole life insurance or VUL polices are much more complicated products, where much more diligence will be needed in selecting a policy. However, when applicable, we’ll make some points about these policies too.

Because the terms that govern whether payout occurs for term life insurance are pretty straightforward (not to be callous, but you either pass away or you don’t), a lot of the grey areas that may come with other types of insurance and whether they determine that you’re eligible for benefits don’t apply when considering term life insurance.

That said, you still want a reputable and financially stable company that has the right product for you. We cover the factors you need to look into below.

PSG Resources

If you are new to learning about life insurance, check out our primer on life insurance for doctors here.

If you need a broker that can help you navigate purchasing life insurance, the sponsors listed on our insurance brokers for physicians page have helped thousands of our members.

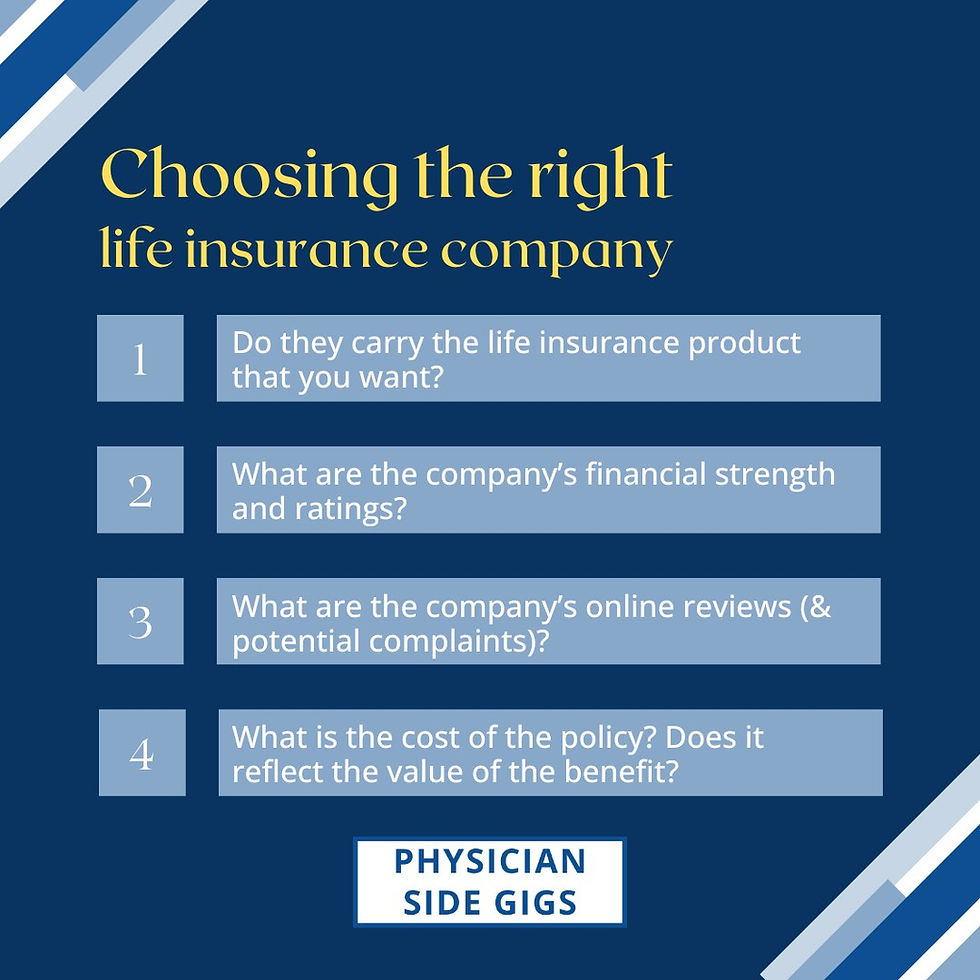

Do they carry the life insurance product that you want?

While term life insurance policies are pretty standard offerings, there may be some companies that have extra features or term lengths compared to other companies. For example, if you’re laddering your life insurance policies, it may be important for you to have an increment that some companies offer and others don’t, like a 15 year option. Similarly, you may want a policy that doesn’t require a medical exam, or that offers options for conversions to a permanent life insurance policy (we’re not necessarily always fans of this, but you may have your reasons for wanting it).

Learn more about purchasing life insurance here.

What is the financial strength of the life insurance company, and what are its ratings?

This is perhaps the most important thing to look at once you’ve determined that they have the policy that you’re looking for. You need to make sure this company is going to be around to be able to pay out when you pass away. Remember that this could be 30 or even 50 or more years from now depending on when you buy the policy. That may sound scary, because we know a lot can happen in that amount of time, but know that there are backup plans available if a company does encounter financial difficulties. Regardless, though, you’d rather not have to navigate those if you don’t have to.

Life insurance companies are rated, and it’s important to look at these ratings. AM Best is a popular benchmark rating system cited by insurance brokers, which takes into consideration the company’s ability to pay out its claims based on money and stability. Ideally you work with a company that has an A++ or A+ rating. Anything below an A should raise red flags.

What is the cost of the policy, and does the price reflect the value of the life insurance benefit?

Ultimately, most people pick whatever policy is the cheapest based on the quotes they are provided by their life insurance broker, provided that the company has a solid rating. That said, you also want to make sure you’re comparing apples to apples when looking at the costs of the policy. Things to make sure you consider include:

Can the policy be cancelled or are there any unusual conditions on the policy?

Is the annual premium guaranteed or can it go up? As an aside, this is where a lot of medical society plans suffer, and where you should exercise caution with medical society policies. This article is about the downsides of buying disability insurance through a medical society, but many similar cautions apply for life insurance

If it’s a permanent life policy, look closely at the fees and other terms and conditions. How does the cash value grow, etc.? Is there an option to stop paying premiums at some point? As we said earlier, discussion of picking a permanent life insurance policy is beyond the scope of this article, but at minimum, make sure you understand the details of the policy when comparing it to others.

Do a quick search for reviews and complaints of the life insurance companies you’re leaning towards

While you likely won’t deal with the life insurance company you pick much after you purchase the policy unless you want to change some of the terms, your heirs will have to deal with them. Do them a favor and look at the reviews in regards to how hard it is to claim the benefit, get in touch with the company, or otherwise make changes or get customer service. Sources to look at include J.D. Power customer service reviews or complaint data with the National Association of Insurance Commissioners (NAIC).

Pay attention to reviews about claims being denied, how smooth of an experience people had in payouts, an unusual number of reports of disputes, or other patterns which may sway you towards or against a particularly company.

Are term life insurance policies really that different from each other, and how do I purchase life insurance?

Honestly, not really, as long as the company is financially stable and the reviews are good. This is one of the more straightforward insurance decisions you’ll make, and probably the one you’ll need the least handholding for (especially compared to something like disability insurance which has so many different options and features).

Once you make the decision that you need to purchase a life insurance policy, the steps are pretty straightforward.

Contact a life insurance broker and get quotes across the many companies selling life insurance, rather than individually contacting each life insurance company. This doesn’t cost you anything, and they can help you navigate the process of choosing how much benefit you need, how to ladder policies, and any questions you may have about how to answer questions on your application. They may also have perks or discounts, and can show you how each of the companies stacks up against each other in regards to price, ratings, and more.

Research what you need to in terms of reputation and financial stability.

Pick the cheapest policy that meets the criteria that are important to you and provides the benefits that you need. Term life insurance costs are generally pretty close to each other from company to company, so it’s more important that you have the right type of policy and coverage with a company that is financially stable.

That’s it. Buy it young to get the cheapest prices, and to ensure that nothing pops up on your medical record that precludes you from qualifying!

Related PSG resource:

Conclusion

As you can see if you’ve ever shopped for other types of insurance with lots of different options, purchasing term life insurance is relatively straightforward compared to those. While it’s always important to do your due diligence, at the end of the day, as long as you go with an established major carrier with a strong rating and reputation, it may just come down to who offers the best price and plan for you.

Additional personal finance and life insurance resources for physicians

Sign up for our weekly newsletter for alerts about upcoming related free webinars, additional educational resources and more.

Related PSG resources: